hankyoreh

Links to other country sites 다른 나라 사이트 링크

[News analysis] What’s behind S. Korea’s explosive increase in household debt?

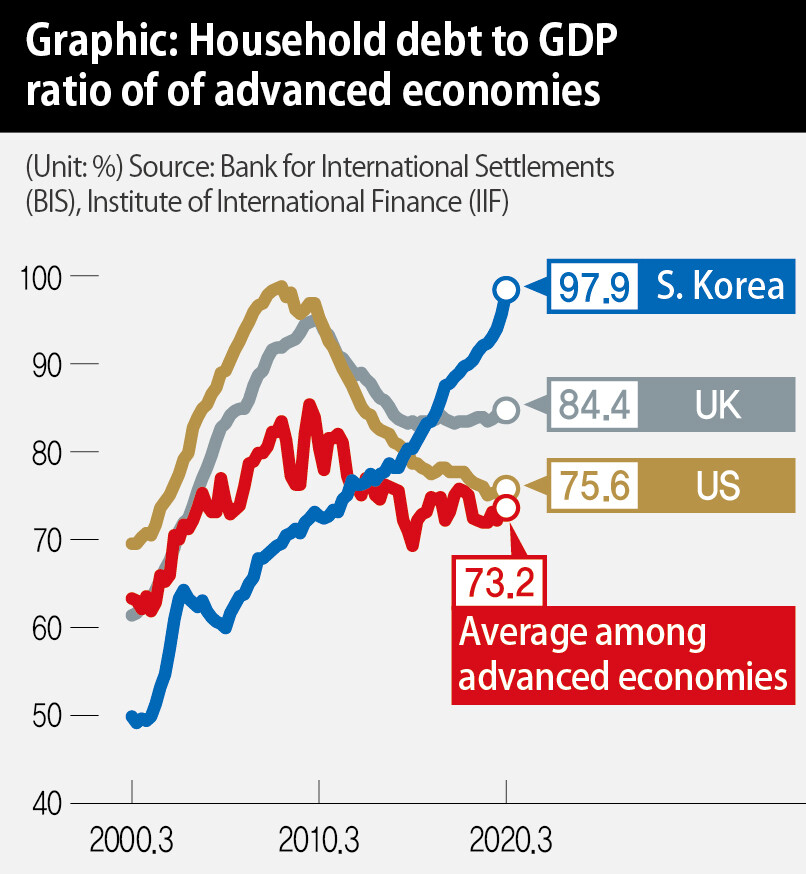

It has been around four to five years since the ratio of South Korea’s household debt to economic scale rose to become the world’s highest. In late 2014, the ratio of household debt to gross domestic product (GDP) crossed the 80% threshold, passing the US’ 79.7%; by mid-2016, it had surpassed the UK’s as well.

A direct contributing factor was a major loosening of housing loan regulations spearheaded by then Deputy Prime Minister for the Economy Choi Kyoung-hwan during the Park Geun-hye administration. In his inaugural address on July 16, 2014, Choi asserted the need to “quickly reform outdated real estate market regulations that are like wearing summertime clothes in the middle of winter.” A week later, he announced the so-called “July 24 measures,” key elements of which included raising banks’ loan-to-value (LTV) ratio for housing by 20 percentage points from 50% to 70% and loosening debt-to-income (DTI) ratio restrictions by 10 percentage points from 50% to 60%. This was the opening salvo for policies that encouraged people to rack up debt in order to purchase homes.

It was around the same time that South Korea’s household debt began approaching a critical point. Researchers at the Bank for International Settlements (BIS) have estimated that the ratio of household debt to GDP begins to exert negative influence on the economy once it passes 85% -- a level that South Korea’s passed for the first time in the third quarter of 2016. During the Roh Moo-hyun administration (2003-08), skyrocketing housing prices fueled a widespread perception that household debt had become a major issue, but even during that administration, the ratio was in the high 60-70% range. It would go on to pass the 70% threshold in the second quarter of 2008, before reaching the 80% mark six years later in the fourth quarter of 2014.

The problem is that the trend of increase has continued even under the Moon Jae-in administration. In the time since Moon took office, the ratio has risen by nearly 10 percentage points. Starting at 88.3% in the second quarter of 2017, it passed 90% in 2018 as rising housing prices resulted in an increase in loans; as of the first quarter of 2020 it had reached 97.9%. Household loan demand has grown since the second quarter amid the combined effects of rising housing prices and the COVID-19 pandemic. With a negative economic growth rate predicted for the year, the ratio is very likely to pass 100% by year’s end.

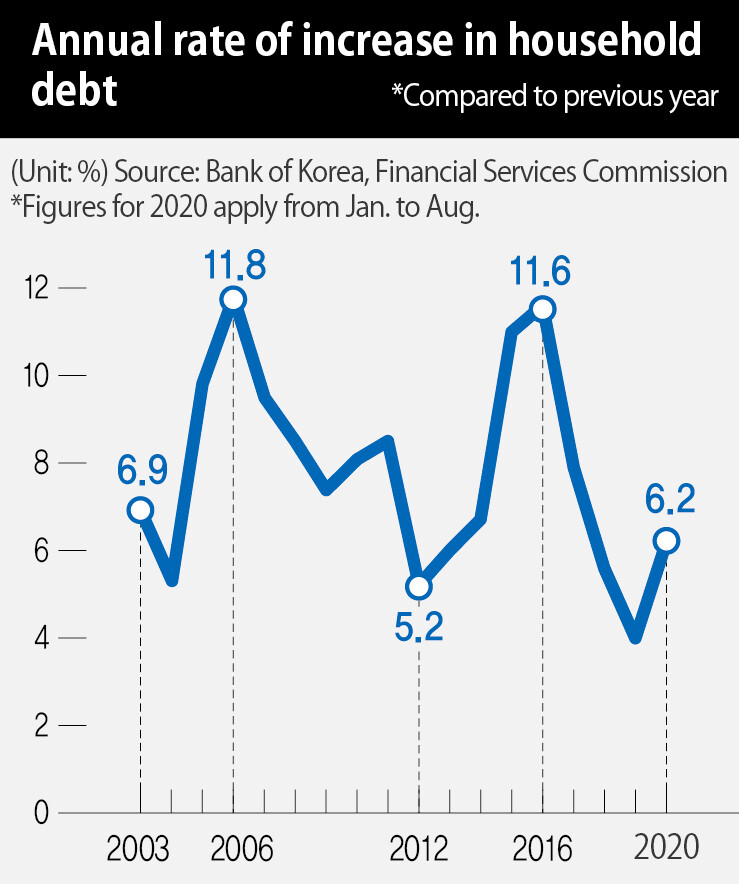

The administration’s target has been to achieve a “soft landing” for household debt by keeping the current economic growth rate lower than the rate of increase in household loans. Its reasoning is that reducing loans in a short period of time could result in major side effects. Indeed, after reaching double-digit levels in the 11-12% range during 2015 and 2016, the rate of increase in housing loans had fallen to 5.6% in 2018 and 4% in 2019. But the eruption of the pandemic turned that situation around -- with a 6.2% rate of increase already as of August this year. This explains the level of newfound urgency surrounding household debt management.

Excessive household debt levels have a negative effect on economic growth as they lead to curtailed consumption. Deepening financial struggles for families faced with critical situations raise the likelihood of financial anxiety. An unanticipated domestic or overseas shock wave could serve to touch off a major crisis. Jang Min, a senior research fellow at the Korea Institute of Finance, observed, “Most global financial crises have been the result of a housing price bubble growing due to increased household credit, and an increase in household insolvency as that bubble collapses.”

Subprime mortgage loans the main culprit behind 2007-2008 financial crisis

A case in point in the financial crisis that erupted in 2007-2008, triggered by subprime mortgage loans. After passing the 85% mark in 2004, the ratio of household debt to GDP in the US had continued to increase, reaching 98% at the crisis’s peak in 2008. Only after that financial crisis had hit did the process of “deleveraging” begin. The ratio fell below the 90% mark as of 2011; by 2014, it was down below 80%. It was an intensely painful process that saw many people driven out of their homes as they were seized by creditors.

Financial authorities recognize the seriousness of the household debt issue, but insist that South Korea is “relatively safe” because the increase in debt has been centered mainly on people with high incomes and strong credit. But apartment prices in the Seoul Capital Area (SCA) have recently reached levels high enough to create a burden even on high-income, high-credit demographics. This means more people who would find themselves drowning in debt if an unexpected shock comes along from within or outside to send housing prices plummeting and interest rates rising.

By Park Hyun, staff reporter

Please direct comments or questions to [english@hani.co.kr]

Editorial・opinion

![[Guest essay] Maybe Korea’s rapid population decline is an opportunity, not a crisis](https://flexible.img.hani.co.kr/flexible/normal/500/300/imgdb/original/2024/0430/9417144634983596.jpg "[Guest essay] Maybe Korea’s rapid population decline is an opportunity, not a crisis") [Guest essay] Maybe Korea’s rapid population decline is an opportunity, not a crisis

[Guest essay] Maybe Korea’s rapid population decline is an opportunity, not a crisis![[Column] Can Yoon steer diplomacy with Russia, China back on track?](https://flexible.img.hani.co.kr/flexible/normal/500/300/imgdb/original/2024/0430/1617144616798244.jpg "[Column] Can Yoon steer diplomacy with Russia, China back on track?") [Column] Can Yoon steer diplomacy with Russia, China back on track?

[Column] Can Yoon steer diplomacy with Russia, China back on track?- [Column] Season 2 of special prosecutor probe may be coming to Korea soon

- [Column] Park Geun-hye déjà vu in Yoon Suk-yeol

- [Editorial] New weight of N. Korea’s nuclear threats makes dialogue all the more urgent

- [Guest essay] The real reason Korea’s new right wants to dub Rhee a founding father

- [Column] ‘Choson’: Is it time we start referring to N. Korea in its own terms?

- [Editorial] Japan’s rewriting of history with Korea has gone too far

- [Column] The president’s questionable capacity for dialogue

- [Column] Are chaebol firms just pizza pies for families to divvy up as they please?

Most viewed articles

- 1After election rout, Yoon’s left with 3 choices for dealing with the opposition

- 2‘We must say no’: Seoul defense chief on Korean, USFK involvement in hypothetical Taiwan crisis

- 3First meeting between Yoon, Lee in 2 years ends without compromise or agreement

- 4Why Kim Jong-un is scrapping the term ‘Day of the Sun’ and toning down fanfare for predecessors

- 5[Guest essay] Maybe Korea’s rapid population decline is an opportunity, not a crisis

- 6Under conservative chief, Korea’s TRC brands teenage wartime massacre victims as traitors

- 7Two factors that’ll decide if Korea’s economy keeps on its upward trend

- 8Months and months of overdue wages are pushing migrant workers in Korea into debt

- 9Noting shared ‘values,’ Korea hints at passport-free travel with Japan

- 10AI is catching up with humans at a ‘shocking’ rate